Many founders imagine the IPO: the ticker symbol, the opening bell, the press release, but in reality, most Health Tech startups exit through acquisition. While only five Health Tech companies completed an IPO in 2025,1 Health Tech M&A has been accelerating. Per Rock Health,2 U.S. digital health M&A grew 61% year-over-year in 2025. This M&A activity is global: according to an analysis conducted by Aytza, the U.S. accounts for just 55% of all deals across 2025 and Q1 2026.3

M&A is the most likely outcome for most startups, so founders should strategically position their company accordingly and as early as possible. Waiting until the business needs an exit leaves founders in a weaker position with fewer options. So what can founders do to be successful in the M&A market? What buyers should they focus on? What strategy and tactics should they engage in?

To answer those questions we dug into the data and conducted an analysis on all Health Tech M&A deals globally from 2025 through Q1 2026. A few things we explored: Who are the acquirers, what do they choose to acquire, and why?

Our analysis categorized acquirers into types and also identified publicly disclosed rationale for the acquisition (shared via press releases or commentary to the press). Of the close to 500 deals we analyzed, we were able to find rationales for 93% of them. We augmented that information with qualitative conversations with founders on both sides of the M&A table, as well as investors.

Understanding Health Tech Acquirers

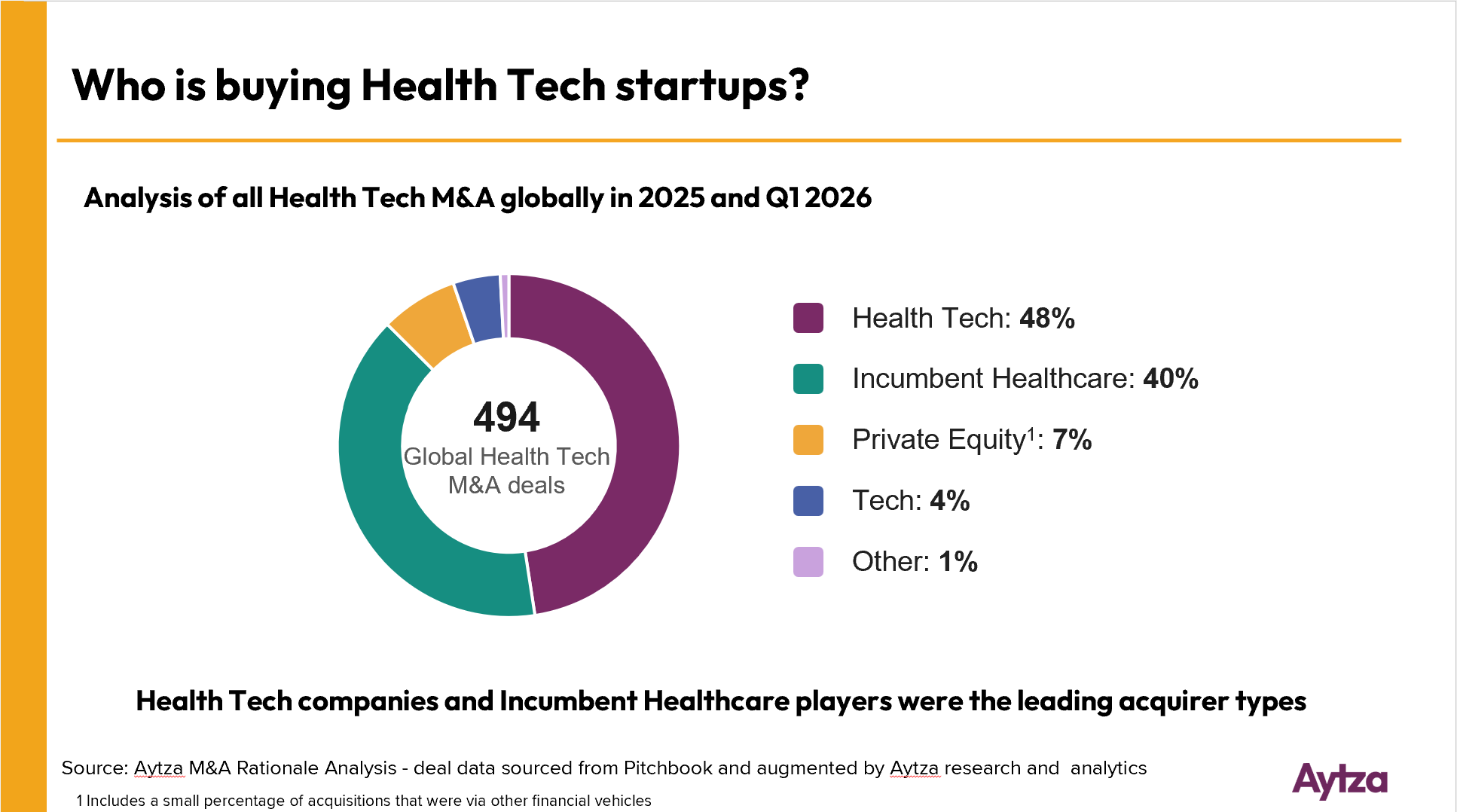

Who is buying?

Globally, the top three acquirer types are Health Tech startups (48% of deals), Incumbent healthcare companies (40% of deals), and Private Equity (PE)4 (7% of deals).

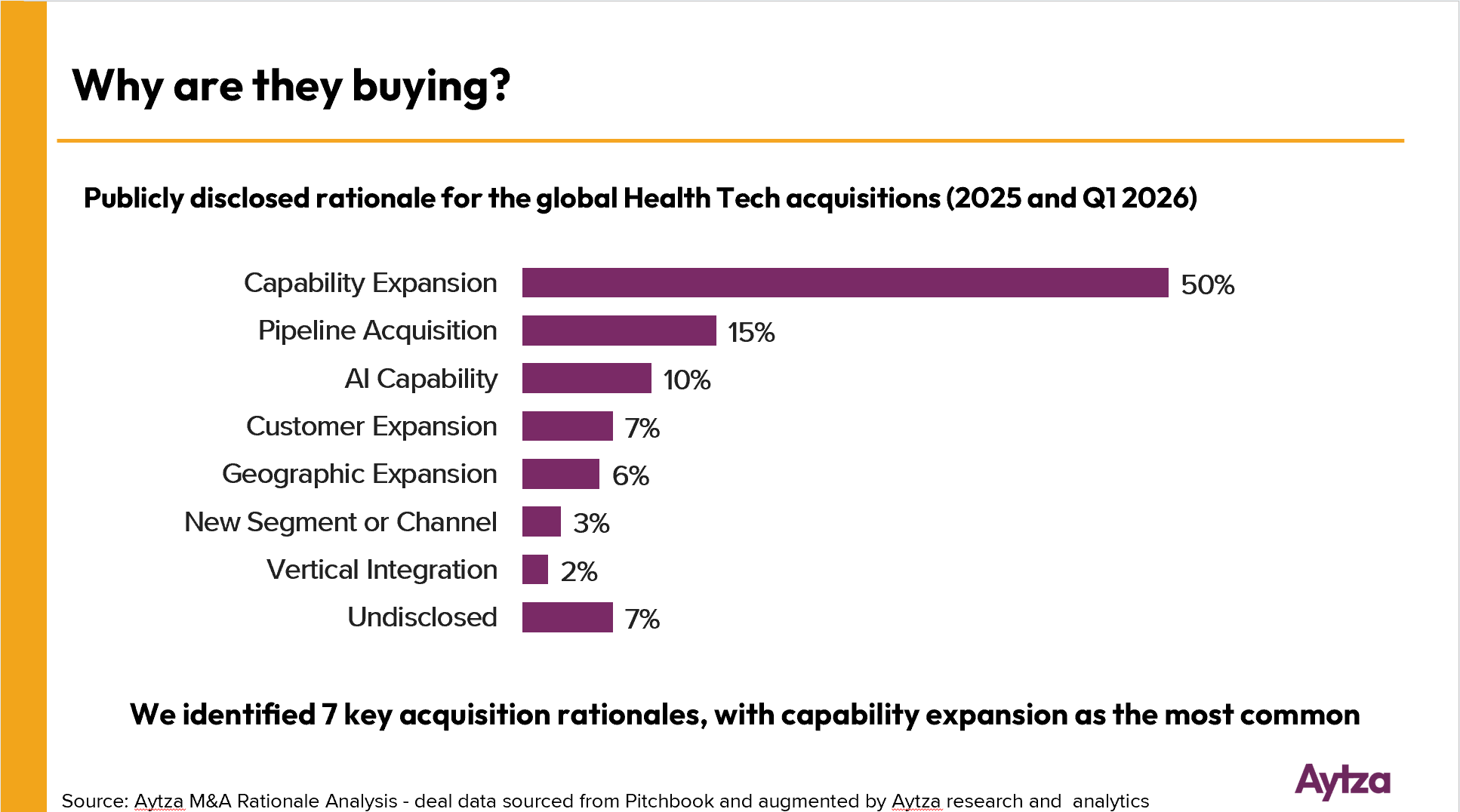

Why are they buying?

Based on our identification of publicly disclosed rationale for the nearly 500 companies, we identified seven primary motivations for acquisition

1. Capability Expansion - Acquiring an adjacent product line, service, specialty, or capability

2. AI Capability - Acquiring AI technology to modernize the business’s product or operations

3. Pipeline Acquisition - Adding a similar product, or IP asset to the buyer's existing development or commercial engine

4. Customer Expansion - Buying new customers of the same type

5. Geographic Expansion - Acquiring as a means of entering a new country or region

6. New Segment or Channel - Gaining access to a new customer type or GTM channel

7. Vertical Integration - Taking ownership of an up- or down-stream stage of the value chain

Roughly half of all deals are Capability Expansions with buyers motivated to add neighboring products, services or specialties rather than building it themselves. The second most frequent motivation category is Pipeline Acquisition in which an asset is added to an existing development or distribution pipeline; somewhat surprisingly, AI came in third with only 10% of companies identifying it as a key rationale, although it was 18% of the secondary rationales mentioned. Other notable rationales, such as enabling Customer Expansion, Geographic Expansion, New Segment or Channel, and Vertical Integration, trailed at single digit percentages.

Interestingly, there are key motivational differences for acquisition across the primary buyer types. For example, 57% of Health Tech acquirers were motivated by Capability Expansion, while just 44% of Incumbents cited that rationale. More striking, for AI capability, 15% of Health Tech companies mentioned this as their primary motivation, while that was only true for 6% of Incumbents. Even when the motivation is similar, each buyer type approaches acquisition differently using distinct on-ramps and assessment criteria.

Next we’ll walk through each buyer type and their unique motivations in detail. Having a detailed understanding of these acquirer types is important, as knowing the makeup of your potential buyer(s) can be the difference between a distressed sale and a strategic win. Then we’ll offer guidance on how to strategically position your company to attract those buyers and conclude by explaining how to avoid the most common M&A pitfalls.

The Three Primary Acquirer Types & What They Want

1. Health Tech Organizations

Health Tech buyers are the most common acquirer type, representing 48% of all M&A activity globally during this timeframe. They are typically more mature startups who are primarily growth-motivated, buying capabilities and scale rather than (or alongside) organic expansion. That scale can be created via multiple levers: Capability Expansion, which is the largest motivation for this buyer type at 57%; Geographic Expansion (7%); Customer expansion (6%); and New Segment or Channel acquisition (5%).

Preventative health company Superpower’s acquisitions during this timeframe are a good example of Capability Expansion. They purchased women's hormone health platform Feminade in January 2025 followed by at-home diagnostic provider, Base, in May 2025.5 Superpower CEO Jacob Peters explained the motivation behind the Feminade acquisition by pointing to the inadequacies in women’s healthcare and how “Feminade’s remarkable growth and deep expertise in women’s health make them the perfect partner to help us close this gap.”6

Following a different motivation, on Aytza’s CEO Pajama Time Podcast, Transcarent CEO Glen Tullman shared that his primary rationale for the company’s April 2025 acquisition of Accolade was Customer Expansion. Through that acquisition, Transcarent was able to rapidly roll out their superior technology across Accolade's large customer base, positioning the company for massive growth.7

Health Tech companies’ second highest motivation was accessing AI capabilities; while the desire for AI tooling was higher than incumbents, it was still only the key rationale for 15% of acquisitions. At least for now, Health Tech buyers are still more motivated by scale (capabilities, geographies, customers, and segments) than AI. Healthcare Growth Partners said it well, “the majority of deals continue to center on mature, pre-AI or transitioning AI businesses with durable customer relationships, proven revenue models, and clear opportunities to apply AI to improve performance.”8

How do these acquisitions come about?

The Health Tech acquirer route can be quite varied, with some companies focused on a concerted capability expansion playbook, acquiring multiple companies to grow, while others act opportunistically to fill capability gaps. We often see a “nesting dolls” scenario in Health Tech where one Health Tech acquires another and then itself gets acquired.

This is what played out in the case of Thirty Madison. Thirty Madison Co-founder and CEO Demetri Karagas shared that they acquired Nurx and Pill Club to pair Thirty Madison’s operational efficiency with the seller’s insurance capabilities to leapfrog the business to the next stage of growth. Notably, those acquisitions made Thirty Madison attractive for acquisition by RemedyMeds in September 2025. Karagas noted, "I don't think we would have gotten to this more diversified platform that we became that ended up being really interesting to a company like RemedyMeds if we wouldn't have [completed those acquisitions]."9

The key to working with Health Tech company acquirers is to stay flexible and nimble as these deals can happen fast and change shape as they go. For example, Validic CEO and Co-founder, Drew Schiller, initially passed on the company he later acquired, circling back several months later after pivoting their strategy to an ownership model.10 The road to acquisition with this buyer type is often not a straight line.

2. Incumbents

Incumbents are the legacy healthcare players: payers, health systems, pharma, PBMs, and medtech. They were the acquirers in 40% of all global health tech deals across 2025 and Q1 2026.11 They are deeply entrenched in their specific markets and often use strategic M&A as their innovation pipeline, acquiring clinical innovation and new technology.

Like Health Tech organizations, Incumbents are largely motivated by expanding their capabilities, with that being the primary motivation 44% of the time. Their next leading motivation is Pipeline Acquisition (28%), in which they are adding a new product, device, or IP asset to their existing commercial engine. For example, diagnostics and life sciences company Natera explained their motivation to acquire Foresight Diagnostics for $450 million: to “combine Natera’s leading commercial and operational infrastructure for the delivery of personalized MRD testing with Foresight’s unique phased variant technology and leadership in lymphoma.”12

Incumbent buyers also sometimes use acquisitions to support Customer Expansion (7%), Geographic Expansion (6%), and Vertical Integration (4%). Interestingly, accessing a New Segment or Channel does not appear as the primary rationale in any of the Incumbent deals over this timeframe.

While AI Capability was listed as the primary motivation in only 6% of cases, our analysis showed that the largest AI-capability motivated acquisition was by an Incumbent. Life sciences and diagnostics incumbent Danaher acquired medical technology company, Masimo, for $9.9B. Danaher's EVP for Diagnostics, Julie Sawyer Montgomery, explained the rationale, saying "Masimo's advanced sensor technology and AI-enabled monitoring bring powerful new capabilities to our diagnostics portfolio."13

How do these Incumbent acquisition deals come about?

Incumbents actively derisk their purchases by acquiring what they already know — a “try before you buy” approach. They often engage in partnerships that, when they go well, lead to acquisition as a next step. Other times, they will invest in companies via their CVC arms to get a toe in the door and later on acquire. Given that process, late stage or cold outreach rarely drives Incumbent M&A.

3. Private Equity

While PE accounts for a small percentage of M&A activity — 10% of U.S. digital health M&A deals in 2025, and 7% in our global analysis — this group’s participation is on the rise: PE health tech spending rose 600% from 2024 to 2025.14 PE firms are the most purely financially motivated of the acquirer types.

PE firms focus on buying businesses with strong fundamentals, building unified solutions, or acquiring a chain of similar companies. They often acquire an anchor company then roll up adjacent ones to build a scaled platform worth more than the sum of its parts.

This group evaluates health tech acquisitions through a different lens, looking for:

- Predictable revenue and cash flow.

- Growth rate with a meaningful margin profile and EBITDA multiples.

- AI as a margin-and-growth lever — increasingly seeking AI-native startups to pair with legacy healthcare players.

For example, in May 2025, PE company New Mountain Capital acquired and combined SmarterDx, Thoughtful.ai, and Access Healthcare into a new entity, Smarter Technologies, an RCM automation and insights platform. New Mountain's then-Managing Director Matt Holt said their approach was to: "identif[y] the market leaders across the most important areas of agentic-AI, machine learning and clinical data, and large-scale automation in the three companies and…combin[e] them to create the innovation leader of the sector."15

How do these PE acquisitions come about?

These deals tend to be much more structured, often orchestrated by a banker or investor, and include an extensive diligence process. Expect little prior connection between the acquirer and acquireree prior to the acquisition.

How to Position Your Business for Successful M&A

Build a sound, profitable business

A founder’s north star and key focus should be on building a fundamentally strong, profitable business that solves a real problem for a big enough market. Despite being prepared for acquisition, don’t build based on what you believe a potential acquirer would want . Dan Vahdat, CEO and Founder of Huma, who has made five acquisitions, guides founders to “ stay focused on building strong businesses rather than trying to predict M&A trends.” Founders should zoom in on what they can control – business fundamentals, the revenue model, customer relationships – rather than “building solely for acquisition or IPO,” Dan says. He goes on to explain that a strong business creates real optionality where founders can decide to exit or not based on what’s in the business’s best interests.16

Identify the best buyer type fit

Founders should take a step back and identify the state of their company – business model, stage, revenue, customers, team, and technology. Assess each area of your company as a potentially purchasable asset. Then think through which acquirer(s) would benefit from each element of your business independently and as a whole. Is your value primarily in your product, data, employees, customer relationships, recurring revenue and EBITDA potential, or something else? Be broad-minded in your thinking, as many companies have something of worth to more than one acquirer type.

Factor in what range of acquisition price you are targeting given the capital your company has raised and the value of what you have built. A $50M exit and a $500M exit draw very different buyer pools. Identify which category of acquirer is most likely to be a fit for your company given all of those elements.

Identify potential buyers & build relationships

With the key buyer type(s) in mind, founders should build a targeted list of relevant potential acquirers. Include the vendors and partners you have worked with in this list of possibilities as well. Once you have that target list, focus on relationship building. Develop relationships via board and investor introductions, conferences, founder events, and spending time engaging with key customers and vendors.

Founders who build long-term relationships early on in the life of their business have a structural advantage, especially when exiting to Health Tech or Incumbent buyers. Wheel CEO and founder Michelle Davey said it well: "One of the things I have learned in M&A is very few times somebody is going to buy something from you or you're going to buy something from them that you've never used, or where you're not deeply embedded. Those relationships really matter — because that may either be your home in the long term or you may be acquiring something."17

Key pitfalls to watch out for in M&A

Even with a strong understanding of M&A, founders can still get tripped up, impacting the sale, its price tag, or their personal outcome. Here are some common pitfalls to avoid:

Pitfall #1: Believing acquirers are buying your company’s potential

When a startup is raising money from investors, the focus is on the company’s future potential; however, an acquirer will also look at what the company has already accomplished. This difference is most pronounced between VC and PE acquirers. VC invests in future growth potential; PE underwrites a present it expects to optimize. That distinction drives the criteria each brings into an M&A evaluation across numerous metrics, including:

- Growth vs. EBITDA: VC backs the growth story; PE backs cash flow

- Last-round valuation vs. financial history: VC typically bases its valuation off the most recent round; PE works backward from actual financials

- Founder-led vs. founder-independent: VC bets on the founder and founding team; PE prefers a business that can succeed without them

- Power law vs. consistent performance: VC accepts most of their bets will go to zero along with one or two fund-returning home runs; PE is attracted by consistent performers

Pitfall #2: Assuming your technology will get you acquired

Sometimes your tech is the draw. More often it isn’t.

Even if your technology is incredible, think about your company assets holistically to identify all the value levers.

Per Sesh founder Tori Lecomte, Caraway Health acquired Sesh primarily for its therapist network and the therapist acquisition-and-retention program behind it.18 Technology can often be rebuilt (especially in today’s AI coding world); customers, networks, trust, and access are harder to replicate.

Pitfall #3: Waiting to look for buyers until you’re ready to be acquired

Part of your founder responsibilities is to know who can acquire you at all times and consistently build relationships with those targets. Georgie Smithwick, Managing Director at Techstars, advises using this approach, recommending "building relationships with potential acquirers long before a transaction."19 She's seen numerous companies succeed this way. As we’ve mentioned, engaging early with the right acquirer type(s) is a critical overlooked component that can really enable you to influence your company’s exit story.

Pitfall #4: Presuming that selling means you're home free

A founder’s goal isn't solely to be acquired at a good price. It's being acquired on your terms, at a price that reflects what you’ve built and by a buyer who’ll give your product and people a good home. For many founders, selling doesn't mean stepping away: earnouts, lockup periods, and integration responsibilities can mean you are required to take a new job and set of responsibilities that is dramatically different from the startup CEO experience you are used to.

Before you sign on the dotted line, understand the terms of the acquisition. Get clear on some of the biggest questions:

- Will your company and product continue independently? Be merged into the parent business? Be discontinued or stripped for parts?

- What role and responsibilities will you have?

- What happens to company employees?

These issues, and many others, are often negotiable — but only before the term sheet is signed.

Pitfall #5: Not securing your own successful financial outcome

As a founder, you have put years of sweat equity (and often your own capital) into the business you have built. The financial decisions made throughout the years can vastly impact how much you personally earn upon exit. If the acquisition price is lower than the value of the cash invested into the business, the money from the acquisition will be paid out in order of preference. For example, if you took on additional rounds of venture capital with preferred equity, those investors will get paid out first (unless you negotiated a management carveout).

Founders sometimes take on debt financing to extend runway while avoiding diluting themselves via additional VC money; in the case of a sale, however, that debt needs to be repaid first before you can access any of the proceeds of the sale. Lee Shapiro, the managing partner at 7wire Ventures, gives this advice to founders: “Keep your eye on how much ownership you have and what's happening with regard to the preference stack in the business. As you add another layer of capital into the business, that's putting more sediment on top of you that has to be paid off before you start to see a payday.”

The bottom line

Health tech innovation aims to improve as many lives as possible as quickly as possible. Delivering on that at scale often requires the distribution, capital, and infrastructure that only a larger and better resourced organization can provide. Whether the buyer is a Health Tech startup, Incumbent, or PE firm, a thoughtful acquisition can give your business a durable foundation to grow into its full potential.

Deals that serve both buyer and seller don't happen by accident. They're the result of a clear-eyed understanding of what you have to offer that your acquirer wants, deliberate and strategic positioning, dedicated relationship-building, and a consistent focus on building a fundamentally good business.

A good exit is likely your company’s best path to impact. Start planning for it now.

Author: Sari Kaganoff, CEO, Aytza

Thank you to Carly Newhouse, LCSW for her support and collaboration on this article!

Weigh in on what we explore next

Aytza helps Health Tech companies navigate commercialization, growth, and M&A.

Get notified when new insights are published - contact us here

Sources

- Fierce Healthcare, January 12, 2026 - “JPM26: Digital health funding hit $14.2B in 2025, with AI companies taking the lion's share of dollars”

- Rock Health, January 12, 2026 - “2025 year-end digital health funding overview: A tale of two markets”

- Aytza M&A Rationale Analysis - deal data sourced from Pitchbook and augmented by Aytza research and analytics

- Includes a small percentage of acquisitions that were via other financial vehicles; we refer to this combined category as Private Equity in this article

- Fitt/Insider, June, 3, 2025 - “Superpower Acquires At-Home Testing Platform Base”

- Femtech Insider, January 8, 2025 - “Preventative Health Platform Superpower Acquires Feminade to Strengthen Women’s Health Offering”

- Aytza’s CEO Pajama Time Podcast, “The founder who won’t stop” episode

- Healthcare Growth Partners, February 5, 2026 - “AI trends shaping the Health IT Transaction Landscape”

- Aytza’s CEO Pajama Time Podcast, “Building the impossible" episode

- Aytza’s CEO Pajama Time Podcast, “The midnight pivot that became Validic” episode

- Aytza Analysis - deal data sourced from Pitchbook and augmented by Aytza research and analytics

- Natera press release, December 5, 2025, “Natera Acquires Foresight Diagnostics”

- Danaher press release, February 17, 2026 - “Danaher to Acquire Masimo Corporation”

- Rock Health, January 12, 2026 - “2025 year-end digital health funding overview”

- New Mountain Capital press release, May 19, 2025 - “New Mountain Capital Forms Smarter Technologies through Combination of SmarterDx, Thoughtful.ai, and Access Healthcare”

- HLTH Europe panel, “The Exit Factor: Why M&A is on the rise in healthtech”, June 17, 2026

- Aytza’s CEO Pajama Time Podcast, “Killing growth to build a lasting company” episode

- Aytza’s CEO Pajama Time Podcast, “From basements to boardrooms” episode

- HLTH Europe panel, “The Exit Factor: Why M&A is on the rise in healthtech”, June 17, 2026

.png)